Debt is a tool. Ever heard this? Lots of personal finance experts have made this statement, but it kind of stops at that—leaving many wondering what that even means.

There’s more to it and the whole debt as a tool thing needs some explanation. The concept needs to be understood because improper implementation of the strategy can lead to major financial mishaps.

What I’m Not Talking About: Consumer Debt

In good times or bad, consumer debt is never a tool. Someone purchasing a couch or TV on credit and then carrying a balance will never work out well. That’s just plain and simple being in consumer debt–there’s no tool.

If you have consumer debt, get rid of it as quickly as possible. Especially if the interest rates are in the twenties.

Related: The Psychology of Paying Off Bad Debt

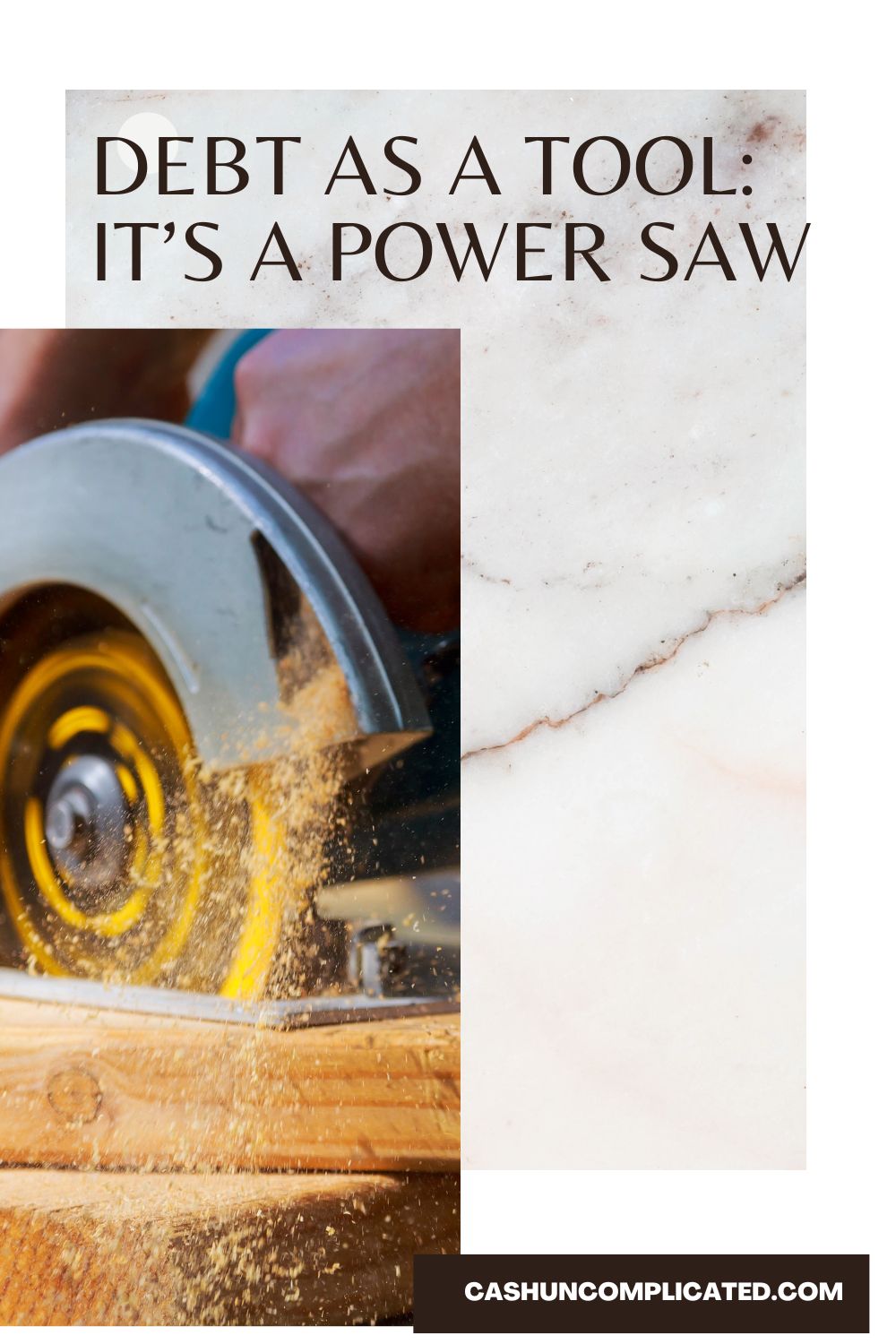

Debt Is a Power Saw

A power saw is a fantastic tool—for someone who knows how to use it. In the hands of an expert, a power saw can help create works of beauty and build houses and skyscrapers.

In the hands of someone like me, a power saw will result in damaged wood at best, missing fingers and limbs at worst. I have no idea how to use a power saw so as soon as I turn it on it becomes a dangerous weapon making it unsafe to be anywhere within 50 feet of me.

At least I know that I have no clue what I’m doing so I don’t try using one on my own.

Debt

The same thing goes for debt. Someone using debt as a tool who really understands it can profit greatly and move faster. For example, a real estate investor who methodically and skillfully fixes up properties and then pulls cash out to buy more assets is likely going to do very well.

However, the person who watches a couple YouTube or TikTok videos on leveraging debt and then tries to implement the strategy is likely to fail. They may even cut off a couple fingers while they’re at it.

Even the Experts Fail

Even an expert using a power saw can fail. So can personal finance experts using debt as a tool. The reality is whether it’s consumer debt or leveraged debt (aka “good debt”), it’s still debt.

Debt means you owe someone else money and have to pay it back. If something happens like a world event like COVID where a tenant may not pay rent for an extended period or a micro event like an eviction or expensive remodel, that debt repayment is harder to fulfill.

Or someone buying stocks on margin. When the market is going up that works great and can greatly increase returns. But when the market goes down, there’s a big problem. It’s a risk that many experts have succeeded and failed in.

Appropriate Risk Assessment

Anyone using debt as a tool has to constantly be assessing for risk. Reason being that you’re literally in debt to a bank, investment group, lender, etc. If you’re not making enough money to pay back the debt, or have a few bad months without proper reserves, you’re in big trouble.

So the wise investor has to assess how much debt should be used, if at all. For example, an investor might have a great opportunity to buy a real estate deal for $100,000 under market value with only 20% down.

Seems like a no brainer right? Not so fast. If the rents don’t cover the debt repayment and more, the deal doesn’t necessarily work as is. Maybe that’s a property to flip or sell after a few months, but you can’t go years and years not being able to cover the debt repayment.

Debt Isn’t All Rosy

In good times, using debt as a tool is easy. Buy a property, or other type of asset, improve it or watch it appreciate with time, and pull money out or take out a loan against it. Then use that money to purchase more assets.

When it works, using debt as a tool is an amazing strategy but when it doesn’t, it’s a huge problem. If it fails, you can literally lose everything.

Conclusion: You Don’t Have to Use a Power Saw or Debt

You can live your life without using a power saw. There’s ways around it like hiring someone or buying an existing property.

Financially successful people can also go their entire life without ever using debt as a tool. There are dozens of other financial tools available, debt is only one of many. It’s a very powerful and sharp tool, but not the only tool in the toolbox.

If you’re not comfortable using one of the sharpest tools available, debt, don’t feel pressured to. While using debt can greatly amplify returns, it’s not essential for financial success. Plenty of people have done fine without it, or using it very sparingly.

So the next time you see someone on TikTok or Instagram preaching about using debt as a tool or OPM (other people’s money), know that it is just one of many strategies. And there’s no pressure for you to use it.

Do you see debt as a tool or should it just be avoided at all costs?